Working Capital

-Looks at the cash needed for the day to day running of

the business / paying bills

-It is more than just cash but focuses on assets that can be turned into cash in the short term e.g. Stock and debtors

-The calculation is current assets minus current liabilities

-A firm would want to see more current assets than current liabilities i.e. It wants to OWN more than it OWES. Otherwise it cannot pay its bills and may go bust / into liquidation

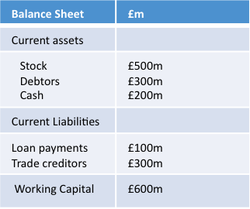

-The table below shows that the company has more current assets than current liabilities and is in a safe position as it should be able to pay its liabilities / bills as they become due

-It is more than just cash but focuses on assets that can be turned into cash in the short term e.g. Stock and debtors

-The calculation is current assets minus current liabilities

-A firm would want to see more current assets than current liabilities i.e. It wants to OWN more than it OWES. Otherwise it cannot pay its bills and may go bust / into liquidation

-The table below shows that the company has more current assets than current liabilities and is in a safe position as it should be able to pay its liabilities / bills as they become due

Working Capital example

L3 Uses of Working Capital

-Identifies negative working capital which may potentially force a firm into liquidation ( i.e. if it OWES more than it OWNS )

-Identifies areas that need improvements e.g. Stock reduction, chasing debtors

L4 – However …

-Remember that it a company has negative working capital it does not automatically mean liquidation. It means that a firm must juggle its payments and try to improve liquidity.

-Also which a firm must try to improve liquidity by eg reducing stock holding or chasing debtors, it must ensure if keeps sufficient stock, and keeps a good relationship with its suppliers.

Conclusion

-Working capital is a useful tool as firms can identify potential cash shortfalls and look at the best management of its current assets, but negative working capital does not means the end of the firm.

-Identifies negative working capital which may potentially force a firm into liquidation ( i.e. if it OWES more than it OWNS )

-Identifies areas that need improvements e.g. Stock reduction, chasing debtors

L4 – However …

-Remember that it a company has negative working capital it does not automatically mean liquidation. It means that a firm must juggle its payments and try to improve liquidity.

-Also which a firm must try to improve liquidity by eg reducing stock holding or chasing debtors, it must ensure if keeps sufficient stock, and keeps a good relationship with its suppliers.

Conclusion

-Working capital is a useful tool as firms can identify potential cash shortfalls and look at the best management of its current assets, but negative working capital does not means the end of the firm.