Budgeting

-A budget is a target for costs and sales

-A firm will always want to exceed the sales target / budget but keep within or below its budgeted costs

-A firm will always want to exceed the sales target / budget but keep within or below its budgeted costs

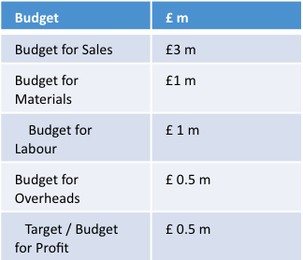

Budget example

-Variance

analysis or budgetary control refers to comparison of a firms actuals ( what

sales were achieved or what costs incurred ) to the budget

-Favourable variances means the company has done better than budgeted e.g. if actual sales were £4m or material costs were only £0.75m

-Adverse variance mean that the company has done worse than expected e.g. Sales were £2m or labour spent £1.5m.

L3 Uses of Budgetary Control / Variance Analysis

-Gives a firm or department a target to work towards-Motivates staff to achieve their sales budgets or find ways to keep costs within budget

-Makes someone accountable / responsible for the spend within a business area

-Useful to compare sales and costs of different outlets / stores/departments

L4 Limitations of budgetary control

-Can demotivate staff if budgets set are not achievable

-Quality can suffer if budgets are too low and departments cut corners

-Sometimes not appropriate to compare different the budgets of different stores due to differing locations etc.

Conclusion

It is necessary for firms to monitor costs to ensure they don’t overspend / lose profits but the targets set must be achievable

-Favourable variances means the company has done better than budgeted e.g. if actual sales were £4m or material costs were only £0.75m

-Adverse variance mean that the company has done worse than expected e.g. Sales were £2m or labour spent £1.5m.

L3 Uses of Budgetary Control / Variance Analysis

-Gives a firm or department a target to work towards-Motivates staff to achieve their sales budgets or find ways to keep costs within budget

-Makes someone accountable / responsible for the spend within a business area

-Useful to compare sales and costs of different outlets / stores/departments

L4 Limitations of budgetary control

-Can demotivate staff if budgets set are not achievable

-Quality can suffer if budgets are too low and departments cut corners

-Sometimes not appropriate to compare different the budgets of different stores due to differing locations etc.

Conclusion

It is necessary for firms to monitor costs to ensure they don’t overspend / lose profits but the targets set must be achievable